Bad Idea: Considering the Debt a Threat to National Security

Over the last decade, the national debt has regularly been framed as a national security issue. Former Chairman of the Joint Chiefs of Staff Admiral Michael Mullen gave prominence to this idea with his headline claim in 2010 that “the most significant threat to our national security is our debt.” This view has been echoed by analysts both championing and critiquing foreign policy approaches that feature sustained military interventions, such as the war in Afghanistan. Many proponents of this view fear that growth in mandatory spending categories, like Social Security, Medicare, Medicaid, and Veteran’s Benefits and Services, as well as interest payments on the debt, is unsustainable and will displace discretionary priorities like military shipbuilding or responding to a crisis. However, while proponents have correctly predicted rising debt, they have been wrong about rising interest payments thanks to persistently low interest rates. Defense cuts and failures to respond to crises were forced by austerity advocates in Congress and not by market conditions. This bad idea has contributed to policies that delayed our recovery from the Great Recession, have undermined our response to the Covid-19 crisis, and threaten to delay the recovery of the U.S. economy.

Those who fear the debt as a threat to national security regularly cite Congressional Budget Office (CBO) projections of an upcoming debt spiral that could lead to a fiscal crisis or expectations of inflation. The CBO succinctly summarizes these fiscal fears: “High and rising debt also might cause policymakers to feel restrained from implementing deficit-financed fiscal policy to respond to unforeseen events or for other purposes, such as to promote economic activity or strengthen national defense.” This serves as the justification for those who view the debt as a national security issue, such as Admiral Mullen who said in 2010: “the strength and the support and the resources that our military uses are directly related to the health of our economy over time.”

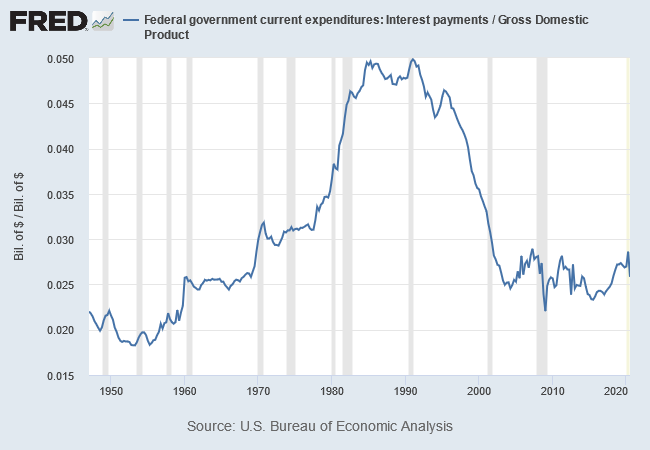

However, these fears that the debt threatens the resourcing of our national security are misplaced. The root of Admiral Mullen’s concern makes sense. Yet using the size of the debt or the ratio of debt to the gross domestic product (GDP) as a proxy for the health of the economy is a misdiagnosis that leads to biased projections. In absolute and percent of GDP terms, the debt has grown over the last decade and especially under the Trump administration. The deficit was projected to hit $1 trillion in 2020 even before the pandemic occurred, but ended up near $3 trillion due to the ensuing economic recession and stimulus measures. Despite all this, there is no debt spiral, and an assessment of the cost of debt as a share of GDP shows that fears that the deficit would crowd out other spending and investment — while justified in the early 1990s — are misplaced. At its peak in late 1995, debt interest accounted for nearly 5 percent of all economic output. Yet the recent peak in the second quarter of 2020 was still under 3 percent and has since dropped. [1]

In a recent white paper, Jason Furman and Lawrence Summers lay out how why the world has changed since the justifiable concern about debt in the early 1990s: “U.S. ten-year indexed bond yields declined by more than 4 percentage points between 2000 and early 2020 even as projected debt levels went from levels extremely low by historical standards to extremely high by historical standards. Similar movements have been observed at all maturities and throughout the industrial world.”

In plain terms, this means that despite large debts, government borrowing remains cheap not just in the U.S. but also in other wealthy countries. Unlike austerity advocates, the economic profession has made note of persistently low interest rates and has adjusted their theories to reflect new evidence, although the sources and implications are still hotly debated. As an alternative to basing fiscal policy on fears of future interest rate hikes, Furman and Summers conclude that even given uncertainty about the future, the economy can sustain a higher rate of investment. Crises like the Great Recession and the Covid-19 pandemic idle unemployed workers and businesses through low demand. The federal government, because of low interest rates and its control over its own currency, can stimulate the economy to get people working in the short term, and can make economy-enhancing investments, such as spending on infrastructure or research and development (R&D), in the long term. In the national security sphere, this would be an excellent time to finance cybersecurity improvements in the defense supply chain and in the larger economy. Likewise, defense R&D spending addresses policymakers’ mandates for defense innovation and has the potential to generate spinoffs for the larger economy, like the development of the internet or GPS technology.

Those focused on reducing the debt have a hard time taking advantage of investment opportunities allowed by market conditions. Framing the debt as a national security imperative has not only failed to prompt thoughtful tradeoffs and compromises in the main drivers of spending on the mandatory side of the budget, but it has also led to rash deficit-reduction policies that failed to contain the debt and harmed the defense enterprise. The 2011 Budget Control Act, passed in response to the debt ceiling and high national debt after the 2008 recession, capped discretionary spending and eventually led to the across-the-board sequester cuts in 2013 triggered by Congress’ failure to reach a compromise. In FY 2013, the Department of Defense faced $37 billion in cuts from sequestration (in then-year dollars) while overall defense spending between FY 2012 and FY 2021 was over $500 billion less than what had been projected in the FY 2012 budget request. Congress ultimately reversed its debt reduction policies by continuously increasing the budget caps on defense and non-defense funds. Whatever the appropriate level of defense spending, these fluctuations are contrary to defense planning principles and encourage mismatches between strategy and spending: for example unclassified contract spending on R&D was slower to recover than similar spending for products and services despite policymakers’ emphasis on the need for innovation.

Concern over the debt and the threat it poses similarly waxes and wanes given political agendas. Senate Majority Leader Mitch McConnell embraced this concern to call for the reduction of the government spending, but helped the Trump administration pass large tax cuts that contributed to the high FY 2020 deficit. Worse yet, debt concerns have played a role in negotiations over the Covid-19 relief packages and have contributed to the delay in passing another stimulus following the expiration of some provisions in the March 2020 CARES Act. A new pandemic relief package is long overdue, as shown by a bipartisan group of top economists that came together nearly a month ago to call for urgent action on further stimulus.

But even if we come together as a nation to address the present crisis, battlelines have already been drawn regarding whether deficit reduction or returning the economy to full employment should take priority during the recovery period. In parallel, the defense budget will be set by what Todd Harrison and Seamus P. Daniels call the “tug-of-war between economic stimulus and fiscal austerity,” These are the wrong battles: rather than viewing policy as a zero-sum competition, we should instead be fighting over what investments are best. Even the best strategists will sometimes identify the wrong center of gravity for a problem, which is why it is vital to update strategies to reflect the state of the world. National security practitioners and long-term planners that have favored austerity should take a hard look at whether their projections over this past decade have held up, and whether the zero-sum arguments focused on deficit reduction have promoted the defense or economic investments they support.

CSIS does not take specific policy positions; accordingly, all views expressed above should be understood to be solely those of the author.

Photo Credit: Courtesy Wikimedia Commons

[1] Back then, Presidents George H.W. Bush and Bill Clinton, together with Democratic Congresses, did take hard measures to bring interest payments under control, but those steps were enabled by the peace dividend from the end of the Cold War rather than forced by concerns about the national security implications of the debt.